Publications

Publications

Partners

Partners

Focusing on CPI inflation is missing the point. Monetary inflation and the declining value of cash are the themes of 2020.

The inflation or deflation debate has been heated since the Global Financial Crisis (GFC) and it’s reared its head again in 2020. During both periods central banks implemented extraordinary monetary loosening measures and analysts feared that this would produce inflation.

Low CPI inflation across the world after 2009 led many to conclude that inflation fears were unfounded. Applying that 2009 to 2016 experience to 2020, one could forecast that inflation will remain contained over the coming years.

This conclusion is overly simplistic and constructing portfolios on the back of it is dangerous. Monetary inflation and the deterioration in the value of cash are big themes for client portfolios in 2020.

The missing ingredient to the inflation or deflation debate is a holistic appreciation of inflation. University economics focuses on the basket consisting the consumer price index (CPI), but this is just one definition of inflation.

A broader definition of inflation is monetary inflation – the amount of new money being created. This is measured through money supply growth, which is dependent on central bank policy and the actions of the banking system. As central banks loosen or tighten monetary policy and commercial banks loosen or tighten lending standards; loans, advances and mortgages tend to increase or decrease. If money supply is growing, then money in that currency is experiencing inflation, and prices – somewhere in the economy – are impacted.

While CPI inflation was contained after the GFC, monetary inflation was strong, and this had consequences. New money must find expression. It could find expression in consumer prices, lifting the CPI basket, but it could find expression elsewhere.

After the GFC, monetary inflation found its way into equity prices, house prices and bond prices. Asset price inflation is the primary explanation for the much-vaunted divergence between the real economy and financial markets.

Why didn’t we see strong CPI inflation? A combination of reasonably weak consumer credit growth, technological innovation suppressing consumer prices, global trade – which allows consumers to receive competitive global prices – and confidence that a currency would continue to hold its value were the main reasons.

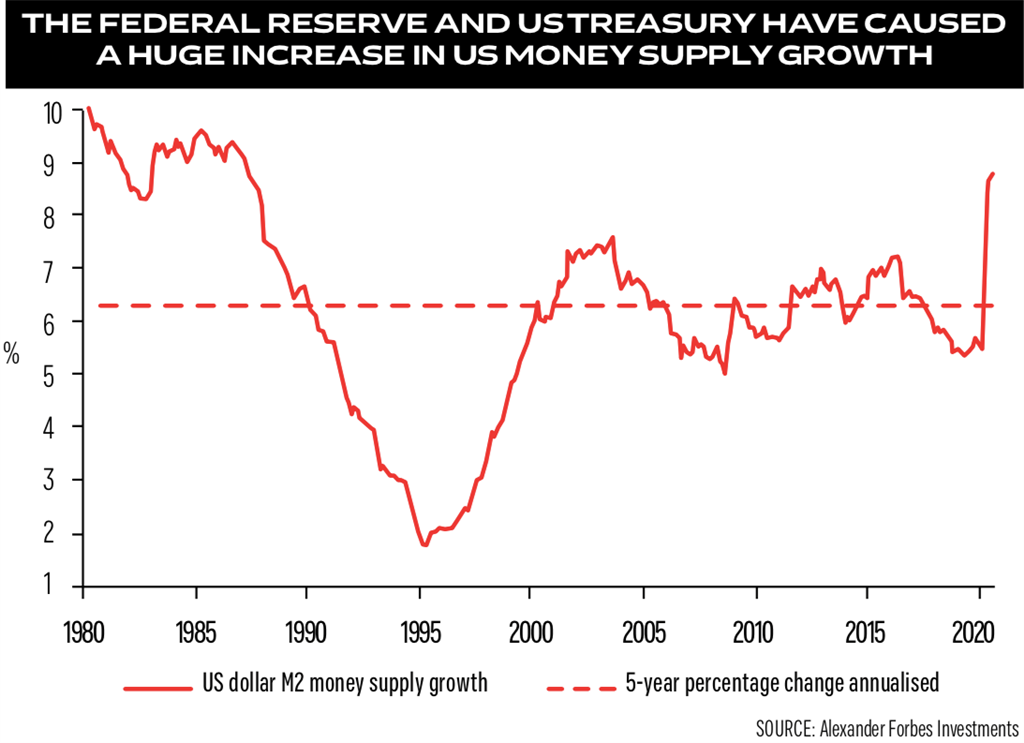

Looking forward, I don’t have all the answers, but we can ask ourselves a few simple questions to deduce the risks and opportunities for 2021 and beyond. Is there monetary inflation? Yes, massive amounts, particularly in the US, which is the world’s biggest economy and biggest financial market (see graph).

Where will all the global monetary inflation find expression?

Authorities are specifically trying to force consumers and business to spend, rather than to save, because they hope this will lift the economy out of recession. This is a badly thought-out policy. Central banks are lowering interest rates to new record lows, ploughing funding into financial markets, and fiscal authorities are implementing direct fiscal transfers to consumers. These policies have an unequivocally negative impact on the value of cash.

This is a critical conclusion because it affects our understanding of everything else in financial markets.

This logic provides a good framework to understand equity markets’ gains in 2020. Equity markets are not pricing a V-shaped recovery, as some might argue. Neither are equity markets looking ahead to a utopian future without the coronavirus. Rather, equities are pricing the impact of monetary inflation on asset prices – asset price inflation.

Investors know that the monetary inflation will have an impact and they’re speculating that equities will be a beneficiary. Various financial markets have been the beneficiary of the extraordinary monetary inflation in 2020, including South African government bonds, global credit markets and precious metals.

Did the SA government become more creditworthy in 2020 to justify lower interest rates on bonds? Of course not. There’s just a lot of money in financial markets that needs to find a home and government bonds appear reasonably attractive, despite a remarkable deterioration in the SA government’s creditworthiness.

The rise in gold is particularly interesting. Gold has no yield. Gold merely acts as a storage vehicle for value over long periods of time. Its rise in 2020 is the marked characterisation of the theme of this article. Focusing purely on the outlook for CPI inflation or deflation misses this crucial information below the surface. No matter the outlook for CPI inflation, monetary inflation and the deterioration in the value of cash are big themes in 2020. Those who merely debate the trajectory of CPI inflation or deflation are missing the point.

Rob Price is head of asset allocations at Alexander Forbes.