Publications

Publications

Partners

Partners

SPONSORED

Cape Town - The concept of retirement has certainly evolved over the last few decades. Thanks to extended life expectancy and a changing idea of what being “old” entails, most people don’t see themselves quietly sitting on a park bench and feeding birds during retirement.

Instead, modern retirement is increasingly seen as an opportunity to explore, start new ventures, become actively involved in your passions and, quite possibly continue making good money while doing so.

But despite this, it is still necessary to save for an income when you’re not working full-time.

Warren Ingram, the director at Galileo Capital, sums up the intention of retirement saving in a modern world: “The goal is to obtain financial freedom as quickly as you possibly can. Nowadays, achieving this goal means being able to work on things you really love, doing the things you want to do…”

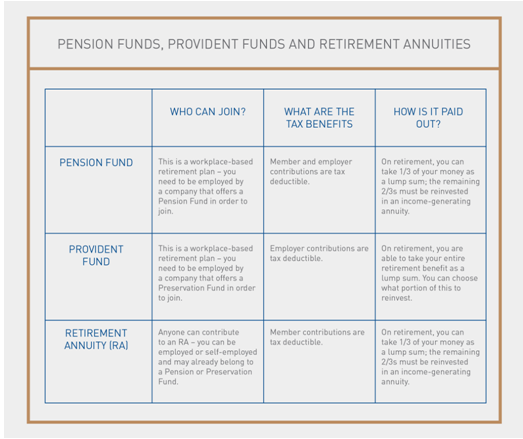

The easiest way of saving for retirement is through vehicles expressly designed for this purpose. The three most common investment vehicles are pension funds, provident funds and retirement annuities.

The most important aim of these savings vehicles is to encourage and enforce regular contributions towards a retirement income that will be accessed at retirement age. (It’s important to note that any lump sums paid out via pensions funds, provident funds and retirement annuities are taxable.)