Publications

Publications

Partners

Partners

Cape Town - Retired investors commonly face the dilemma of either maintaining a certain lifestyle or adjusting it in order to preserve their savings.

Typically the more income one draws and spends today the less is available to create future income. When inflation is added to this quandary, it becomes important to also grow that income over time to retain one’s buying power.

Income specialist company Marriott has researched the sustainable levels of income that retirees were able to draw historically, to better understand the difficulties retirees face and why in retirement you should spend the income and not the capital.

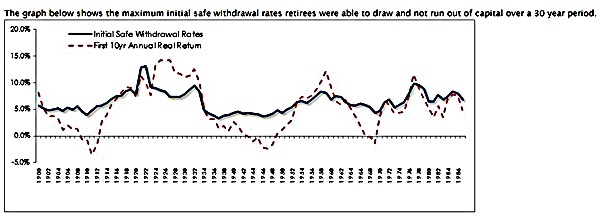

Its research, using returns for SA asset classes going back to 1900, tested how much retirees could safely draw from their savings without running out of capital for 30 years. For research purposes it was assumed each retiree invested R1m in a typical balanced fund (comprising 60% equities, 30% bonds and 10% cash) and drew an annual income that kept up with inflation.

Initial safe withdrawal rates have fluctuated significantly over time. Some retirees were able to start with a withdrawal rate as high as 13%, grow their income in line with inflation and still have a successful retirement - capital that lasted for 30 years.

A closer look at the data revealed that maximum safe withdrawal rates correlated with the first 10-year annual real returns the investor experienced.

Maximum initial safe withdrawal rates retirees were able to draw and not run out of capital over a 30 year period:

In other words, lower maximum safe withdrawal rates coincided with lower real returns and vice versa. This seems obvious, but the difficulty retirees face is that future returns are difficult to predict.

The concern for retired investors today is that market returns are expected to be below average for the next decade, due to demanding valuations combined with lower growth expectations. This suggests many living annuities will come under pressure in the years ahead.

Marriott has two suggestions for retired investors:

Match the income drawn with the income produced

Investors should be aware of how much income their portfolio is generating and try to draw no more than the income produced – thus avoiding capital erosion.

Investments that produce reliable and consistent income streams assist investors to avoid capital erosion over time. If an investor can avoid capital erosion, they can secure their future income.

It is especially important in the early stages of retirement that capital is preserved as far as possible. If investors wish to draw more income than their investment is producing, it should be with the knowledge that they are eroding their capital.

Choose investments which produce consistent income streams that grow over time

Investors not only need to preserve capital, but also need to ensure they protect themselves against the impact of rising living costs over time.

Investments that produce a reliable income stream that grow over time, like equities, are critical for a successful retirement as the income produced from these investments tend to grow ahead of inflation.

By including equities with a reliable growing income stream, investors will be able to ensure growth in income over time. The trade-off of including equities, however, is that an investor’s portfolio will produce less income initially.

Investors need to find the appropriate level of exposure between the different asset classes that will give them enough income and income growth over time.

Marriott suggest that investors examine their situation carefully when considering using capital to supplement their income. It strongly urges investors to preserve capital until they reach a stage in their retirement years when it may become safer to drawdown on capital.

While investors may find it challenging to restrict their annuity income to the income produced in the current low yielding environment, it is preferable to finding that one’s capital has been partially or even completely eroded.

Rather be conservative now than risk having to find another source of income, such as going back to work or having to reduce one’s standard of living at some point in the future.

"The simple truth is, if you spend more than you earn, you will erode your capital and ultimately erode your income. When it comes to investing, particularly in retirement when capital preservation is paramount, this age-old wisdom rings true even today," says Marriott.

SUBSCRIBE FOR FREE UPDATE: Get Fin24's top morning business news and opinions in your inbox.

Read Fin24's top stories trending on Twitter: Fin24’s top stories