Publications

Publications

Partners

Partners

AT UNIVERSITY I was taught that the first principle of retirement savings is to match assets to liabilities and in doing so, generate sufficient capital at retirement to buy a pension.

After all, a retirement fund, if smartly invested, ensures that your old age is provided for and quality of life is maintained.

The reality is, however, that more than half of today’s pensioners have not done enough to ensure this. Recent industry studies indicate that only 6% of South Africans have accumulated enough savings to retire comfortably.

Mirroring global trends, South Africans are living longer and as a result need to work longer or save more to maintain their standard of living.

Experts suggest that for retirement to be met with distinction, a net replacement value of 75% needs to be secured. To achieve this, the appropriate investment strategy is key.

It is also the component that generates most controversy and can range from conservative, balanced, aggressive and member choice to life staging.

These strategies are promoted by providers based on their house views, and choosing one that best suits the first principal goal is not easy.

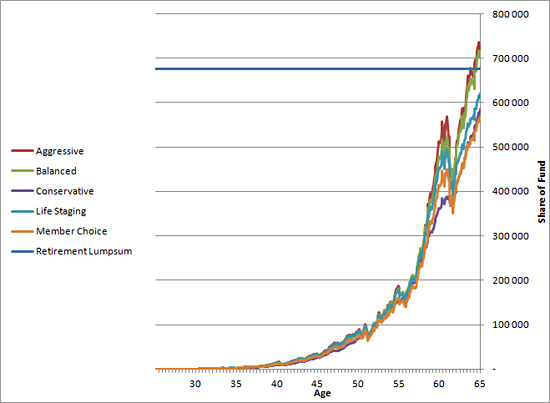

Figure A illustrates the difference between these strategies by considering past performance of the major assets classes based on typical asset allocations and fees.

The model depicts the retirement savings growth secured to achieve a retirement lump sum. In all cases, the member started saving at age 25, based on:

Figure A: A retirement model depicting the return secured by various investment strategies.

The graph yielded the following insights:

The price paid by member choice

The low return achieved by a member choice could be attributed to the higher fees incurred by this strategy. Members are set back further, as they are often ill equipped to make informed decisions.

Often reactive to “market noise”, members ping pong between conservative and aggressive, losing return in the process. For instance, while stocks are falling, human nature is to transfer investments into safer assets.

Had a member done this during the 2008 financial crisis, they would have lost up to 30% of their retirement savings.

Conservative approach, conservative returns

A conservative strategy does not fare much better than member choice. It is incapable of achieving the returns required for a retirement with a high enough net replacement value.

If you invest in conservative assets, you will struggle to generate the returns needed to sustain your quality of life throughout retirement.

Better off with life staging?

Life staging, which according to the model presents a mediocre return, is based on the principle of matching asset allocation to age based on life stages. This strategy suggests an aggressive strategy for younger members and a conservative one for those moving closer to retirement.

While life staging can allow a member to be “better off”, the associated fee often results in a member losing out on performance.

The risk of an aggressive strategy

The calculated retirement lump sum from an aggressive strategy is the highest. In theory, this strategy rewards an investor with high returns.

However, when it comes to balancing risk, there seems to be little gained for the extra risk when compared to a balanced strategy.

Balanced ensures retirement with distinction

A balanced strategy secures a return just below an aggressive strategy – without the risk. Focused on “not placing all your eggs into one basket”, this strategy aims to allocate assets across conservative and aggressive classes. In doing so, it reduces risk and produces a stable, balanced growth.

True to the old adage, “Tomorrow belongs to the people who prepare for it today”, investing in your retirement is the most important investment that you can make. T o ensure that old age is provided for and your quality of life is maintained, retirement savings should be balanced across conservative and aggressive asset classes.

A balanced investment strategy should secure your retirement worthy of distinction – which is a net replacement value greater than 75%.

- Fin24

*Walter van der Merwe is CEO of FedGroup Life. Views expressed are his own.

After all, a retirement fund, if smartly invested, ensures that your old age is provided for and quality of life is maintained.

The reality is, however, that more than half of today’s pensioners have not done enough to ensure this. Recent industry studies indicate that only 6% of South Africans have accumulated enough savings to retire comfortably.

Mirroring global trends, South Africans are living longer and as a result need to work longer or save more to maintain their standard of living.

Experts suggest that for retirement to be met with distinction, a net replacement value of 75% needs to be secured. To achieve this, the appropriate investment strategy is key.

It is also the component that generates most controversy and can range from conservative, balanced, aggressive and member choice to life staging.

These strategies are promoted by providers based on their house views, and choosing one that best suits the first principal goal is not easy.

Figure A illustrates the difference between these strategies by considering past performance of the major assets classes based on typical asset allocations and fees.

The model depicts the retirement savings growth secured to achieve a retirement lump sum. In all cases, the member started saving at age 25, based on:

- Salary at retirement of R120 000 per annum;

- Contribution rate of 14% throughout;

- Annuity rate of 7.5%;

- Salary growth rate of 4% p a on top of inflation; and

- Retirement age of 65.

Figure A: A retirement model depicting the return secured by various investment strategies.

The graph yielded the following insights:

- Aggressive and balanced surpassed the required retirement lump sum saving.

- Other strategies fell short of the mark.

- Conservative and member choice produced the worst result.

- Over the period, there is volatility in performance between the strategies, as expected.

The price paid by member choice

The low return achieved by a member choice could be attributed to the higher fees incurred by this strategy. Members are set back further, as they are often ill equipped to make informed decisions.

Often reactive to “market noise”, members ping pong between conservative and aggressive, losing return in the process. For instance, while stocks are falling, human nature is to transfer investments into safer assets.

Had a member done this during the 2008 financial crisis, they would have lost up to 30% of their retirement savings.

Conservative approach, conservative returns

A conservative strategy does not fare much better than member choice. It is incapable of achieving the returns required for a retirement with a high enough net replacement value.

If you invest in conservative assets, you will struggle to generate the returns needed to sustain your quality of life throughout retirement.

Better off with life staging?

Life staging, which according to the model presents a mediocre return, is based on the principle of matching asset allocation to age based on life stages. This strategy suggests an aggressive strategy for younger members and a conservative one for those moving closer to retirement.

While life staging can allow a member to be “better off”, the associated fee often results in a member losing out on performance.

The risk of an aggressive strategy

The calculated retirement lump sum from an aggressive strategy is the highest. In theory, this strategy rewards an investor with high returns.

However, when it comes to balancing risk, there seems to be little gained for the extra risk when compared to a balanced strategy.

Balanced ensures retirement with distinction

A balanced strategy secures a return just below an aggressive strategy – without the risk. Focused on “not placing all your eggs into one basket”, this strategy aims to allocate assets across conservative and aggressive classes. In doing so, it reduces risk and produces a stable, balanced growth.

True to the old adage, “Tomorrow belongs to the people who prepare for it today”, investing in your retirement is the most important investment that you can make. T o ensure that old age is provided for and your quality of life is maintained, retirement savings should be balanced across conservative and aggressive asset classes.

A balanced investment strategy should secure your retirement worthy of distinction – which is a net replacement value greater than 75%.

- Fin24

*Walter van der Merwe is CEO of FedGroup Life. Views expressed are his own.