Publications

Publications

Partners

Partners

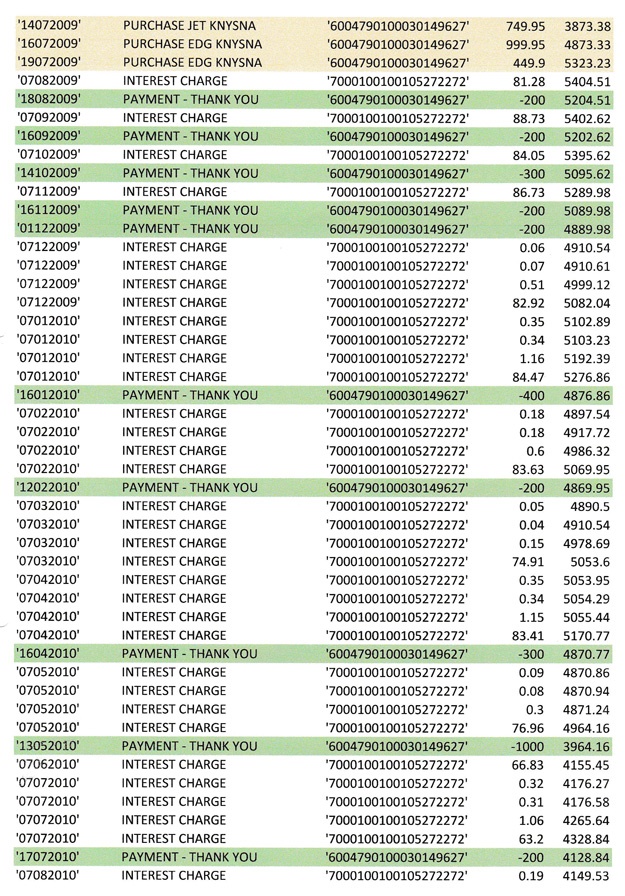

WHEN your only income is a state Disability Grant of R1 500 per month, every rand counts. Ten years ago mentally challenged Leticha Marinana opened a credit account to buy clothes at Edgars, South Africa’s largest fashion group. Over the first three years she bought R10 497 worth of items, then never used her card again. With interest and charges she’s paid back R16 217 in monthly payments from her disability grant, but she was still being harried for a further R4 798.

Leticha is 39 and lives in Knysna on the scenic Garden Route. Not that she sees much of the tourist town voted second favourite city in Africa by Condé Nast Traveler, for Leticha is intellectually disabled and rarely leaves the timber RDP house in Khayalethu South that she shares with her 72-year-old widowed mother.

To pass the days, Leticha does the cooking and watches a lot of TV, the highlight being 9pm on weekdays when she escapes into the fantasy world of the SABC2 soapie Muvhango. It’s a relief from her once-tranquil real life, which has been spinning out of control since she got caught in a debt trap.