Publications

Publications

Partners

Partners

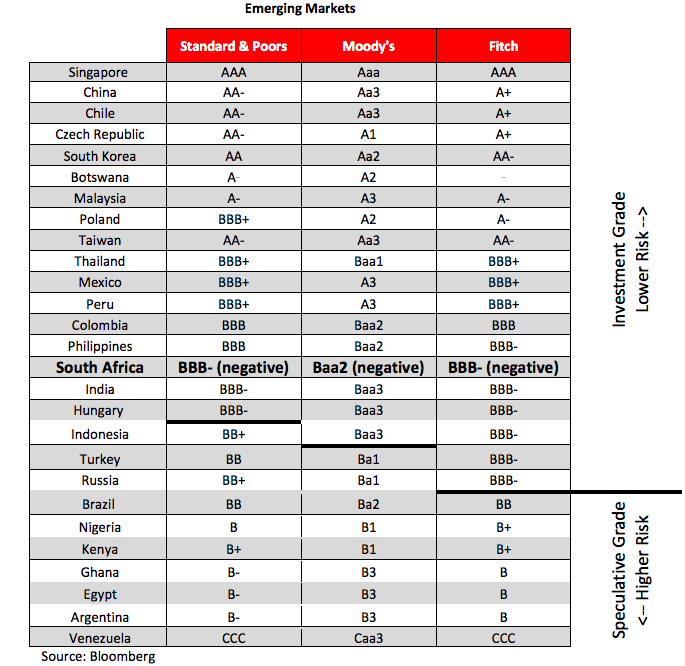

Ratings downgrades matter because they feed into the value of a currency and other assets. South Africa has avoided a ratings downgrade, though there is still the risk of this happening.

Nevertheless, the ratings agencies aren’t the only organisations to watch if you are trying to read the direction of the rand. Azar Jammine, a leading economist, points to the influence that US policies have on the value of the dollar – which reflects in other currencies. Jammine scrutinises the statement from S&P Global Ratings for clues about what is in store for South Africa.

Aside from political infighting within the ANC’s leadership raising eyebrows among investors, there are concerns about serious weaknesses with the country’s economy. These include the shortage of skills, the structural maintenance of a large current account deficit and the insufficiency of capital investment by the private sector.

Expect the fears that the country could be downgraded to dominate talk about the rand well into next year, is Jammine’s message. – Jackie Cameron

By Azar Jammine*

Opinions had been divided about whether or not S&P Global Ratings would decide to downgrade the credit rating on South Africa’s foreign debt from the existing BBB- rating down to BB+.

S&P Global Ratings had assigned a “negative” outlook on the existing BBB- rating, implying that there was a good chance of a downgrade from that rating.

What was particularly important about this was that a BB+ rating would have constituted sub-investment grade as opposed to the current BBB- rating which is considered to be investment grade. The corollary is that investors might have become less willing to purchase South African foreign debt.

Given the large shortfall in the difference between what the country imports and what it exports, viz. the current-account deficit, relative to other similar emerging markets, a decline in the willingness of investors to acquire South African foreign debt could have placed downward pressure on the Rand, with negative consequences for the inflation and interest rate outlook and through this for economic growth more generally.

A week ago the other two main credit rating agencies similarly left their credit ratings on South African foreign debt unchanged. This had the effect in the markets of reducing the probability that S&P would downgrade its rating after all.

Nonetheless, there did remain a residual unease that S&P would go ahead with a ratings downgrade. It therefore did come as somewhat of a relief that it did not do so.

However, US Factors Also Contributed To Rand Strength In the run-up to the S&P announcement, as well as in the immediate aftermath of the announcement, the Rand’s exchange rate strengthened by just under 3% during the latter part of last week vis-à-vis the Dollar.

It is seductive to suggest that this Rand strength was attributable to the absence of a credit rating downgrade on the country’s foreign debt. However, closer analysis reveals that this was not the only factor underlying the strength of the South African currency late last week.

The Dollar itself weakened by just under 1% against other currencies from multi-year highs it had reached earlier in the week. These highs had been based on expectations that the Fed will raise the Fed Funds rate when its Federal Open Market Committee meets next week.

More importantly, the election of Donald Trump as US President, with his commitment to embarking upon huge infrastructural investment spending and tax cuts, has implied that December’s expected rate hike will be followed by several further rate hikes next year and beyond as US interest rates normalise back to traditional levels of around 3%/4% compared with the near-zero levels that prevailed for eight years.

This expectation has caused funds to flow out of assets in other currencies into the Dollar.

However, some of this Dollar optimism was tempered on Friday by the release of the monthly non-farm payrolls data. In recent weeks, favourable retail sales data, coupled with the release of a better-than-expected 3.2% GDP growth figure for the 3rd qtr had been creating the impression that even before Trump took over the presidency, US economic growth was picking up steam.

The path for higher US interest rates was therefore justified even more strongly. Nonetheless, the 178,000 gain in US non-agricultural jobs in November was slightly less than anticipated.

Furthermore, notwithstanding the decline in US unemployment to a nine-year low of 4.6%, the report on US

earnings showed these to be rising a little more slowly than previously anticipated.

On a y-o-y basis, earnings rose by 2.5% in November, down from the 2.8% growth recorded in October, which had been the highest since the global financial recession. This eased expectations that US wage inflation might start rearing its head and in so doing might reduce some of the pressure for US interest rates to rise as steeply as feared.

The resultant weakness of the Dollar added further to the Rand’s appreciation against the greenback for reasons other than the S&P decision.

Some contradictions in S&P analysis

Nonetheless, there were some contradictions in the analysis presented by S&P Global Ratings for why it decided what it did. Whilst it left the key credit rating on South Africa’s foreign debt unchanged, it reduced the credit rating on South Africa’s local currency denominated debt from BBB+ to BBB, i.e. it reduced the gap between the rating on foreign debt and that of the local debt from two notches to one notch.

This is difficult to understand given the high level of liquidity in South Africa’s financial system and its remarkable strength. South Africa’s banking system is one of the strongest of any emerging market.

The concerns with the country lie far more with its ability to attract buyers of its foreign debt to compensate for the shortfall in foreign exchange earnings caused by the large current account deficit.

Secondly, S&P emphasised that the reason why it reduced this credit rating was because the uptick debt to GDP ratio had been rising by 0.7% more than S&P had expected it to do and was likely to continue increasing by more than previously anticipated.

The latter expectation rose from the fact that domestic economic growth was turning out to be less than anticipated.

On the other hand, the ratings agency concluded that a downgrade would occur if South Africa’s growth went into recessionary conditions. The fact is that growth is still positive and despite this, the public debt to GDP ratio still rose by more than S&P had anticipated.

It therefore begs the question as to what the increase in public debt to GDP ratio is that would force the ratings agency to downgrade the rating on foreign debt to junk status.

Also read: Could ratings agencies protect Pravin Gordhan? Analyst assesses downgrade risk

It also raises the question as to whether or not an improvement in economic growth next year to 1.5% or so, in line with expectations, will indeed be regarded as sufficient towards staving off a downgrade to junk status even if such growth is still insufficient to prevent an increase in the public debt to GDP ratio?

Superficially, if the economy grows by less than the budget deficit to GDP ratio, then it means that the public debt to GDP ratio will rise. Given this, the projected budget deficits of between 2.5% and 3.4% over the next three years are likely to be well above the growth rate in GDP of the economy over this period, implying a substantial increase in the public debt to GDP ratio after all.

In light of the concerns which S&P has about the rising trend of public debt to GDP, this ought to be sufficient to compel the ratings agency to downgrade to junk, yet it talks only about downgrading if economic growth is less than zero.

The other question one asks in relation to the consistency of the rationale for not downgrading South Africa’s credit rating to junk status is the emphasis that such a high proportion of South Africa’s government debt is denominated in local currency terms rather than in foreign currency. This has been regarded as a fundamental strength in the economy for many years. Why is it now such a big factor in preventing a downgrade when it has for long been a factor supporting the view that the country does not deserve a downgrade?

Prerequisites for structural reforms needed to sustain higher growth

Insofar as the prerequisites for attaining a higher sustainable growth rate to avoid a downgrade to junk status, S&P highlighted the same factors as those indicated by Fitch and Moody’s a week ago, viz. the need to reduce political infighting in order to avoid distracting attention of the authorities away from addressing the structural weaknesses inhibiting improved growth. S&P also focused on minimising the potential increase in contingent liabilities of SOEs through better management of the latter.

However, over and above these factors, it is insightful that S&P also pointed to the relative absence of capital investment by the private sector as an important inhibitor to growth. It also alluded to insufficient skills development as a further constraint on higher economic growth.

It goes without saying that increased harmony on the labour relations front is also an important prerequisite. In regard to all these factors, the National Treasury has been on a campaign all year to garner support and cooperation between public sector and private sector.

To this end it is called a “team South Africa” initiative between the government, certain labour leaders and 80 CEOs to go on roadshows domestically and abroad aimed at convincing international investors that the country is indeed determined to address the above-mentioned structural impediments to higher economic growth.

Sceptics will nonetheless continue to suspect that much of the initiative focuses on talk and bluster, and that the fundamental resolution of the impasse between those favouring market-oriented solutions to the country’s economic problems and those favouring interventionist solutions, will not be forthcoming. This is the real challenge to avoiding credit ratings downgrades in the future.

Fear of downgrade to junk status next year to continue

In conclusion, it does indeed come as a relief that none of the three credit rating agencies have decided to reduce the rating on South Africa’s foreign debt to junk status.

Even so, the factors which might eventually compel them to make that move, have unfortunately not evaporated. Several challenges still remain, including most importantly the need to uplift South Africa’s sustainable economic growth path.

If indeed recent optimism regarding an upswing in US and global economic growth following the election of Donald Trump as US President materialises, this will assist the domestic authorities in uplifting growth.

However, it remains a huge challenge to try to forge a unified economic policy that carries the support of both the left and market-oriented ideologies in the country. Attempts at achieving this unified approach are likely to be confronted by significant impediments due to political wrangling in the year ahead in the run-up to the ANC’s presidential election Congress in December next year.

It is questionable whether the dearth of capital investment by the private sector which is cited by S&P as one of the inhibitors of higher economic growth, will be able to gain ground in such an environment. Business confidence is likely to remain fragile. Squabbles about leadership issues are likely to be conflated with policies aimed at structural reform.

Accordingly, concerns relating to a downgrade to junk status during the course of 2017, whether for mid-2017 or December 2017, are likely to remain in place. Under such circumstances, one should not be looking for the Rand to make significant further gains in the short to medium term.

- Dr Azar Jammine is the chief economist at Econometrix.

Read Fin24's top stories trending on Twitter: Fin24’s top stories