Publications

Publications

Partners

Partners

The department of trade and industry (the dti) and the National Credit Regulator have set off a bomb in South Africa’s credit industry.

New proposed limits on interest rates and fees were gazetted last week that amount to a kick in the teeth for the unpopular microlending industry, which has been lobbying ferociously for higher legal rates and fees.

The dti proposals would instead do the opposite: slash the rates charged on short and unsecured loans as well as store cards and credit cards – all the main avenues of lending to poor South Africans.

The proposals are also likely to have a knock-on effect on all credit providers, including large banks, especially once the SA Reserve Bank starts raising its repo rate in coming years (see below).

This will be the first review of legal rates and fees since 2007, when the National Credit Act came into full effect.

The largest immediate effect of the dti’s proposals, which are open for comment this month, would be on unsecured loans – where the maximum legal interest rate would instantly fall from 32.65% to 24.78%.

Short-term loans, defined as less than R8 000 for less than six months, will retain their maximum rate of 5% per month, but that will fall to 3% if the same person takes out two loans in a single year.

Credit cards, overdrafts and the store cards issued by retailers – which are in essence credit cards – have a maximum rate of 22.65%, which would drop to 19.8%.

All these rate cuts would immediately change the game for the margins of the credit sector, making much of their debt books illegal unless their rates are dropped.

The proposals also affect the initiation and service fees that lenders can charge.

Where microlenders have been begging for a doubling of the permissible maximum initiation fees to R2 000 per loan, the dti is proposing an almost pointless symbolic increase of 5% to R1 050.

Where the industry had wanted the maximum monthly service fee doubled to R100, the dti is proposing R60.

The proposals are an unequivocal rebuke of microlending industry lobby group Microfinance SA (MFSA), which has been mounting a campaign to get rates and fees adjusted in the opposite direction.

The MFSA position has been that, at the very least, the fees should be adjusted to take inflation over the past eight years into account.

Hennie Ferreira, CEO of the MFSA, calls the proposals “disappointing” and says his organisation will not only make a submission on it but engage with the dti “to understand the rationale”.

The MFSA’s position is that lowering maximum legal rates will instead drive the margins of the credit market into the arms of illegal moneylenders who “are waiting in anticipation”.

Zodwa Ntuli, deputy director-general at the dti for consumer and corporate regulation, said the proposals were the third leg of government’s attempts to fight overindebtedness.

The first was to amend the National Credit Act to introduce more stringent affordability tests. The second involved ongoing moves to stop credit providers from making their money through additional, often hidden, credit-insurance sales.

The proposed changes to maximum rates and fees aimed to “balance access and affordability”.

“As much as we want people to have access to credit, they must be able to afford it. Otherwise, they end up in a debt cycle from which they may never escape,” Ntuli told City Press.

The National Credit Regulator’s spokesperson, Lebogang Selibi, said the proposals were informed by “the growth of unsecured credit agreements over the past few years, the current levels of consumer overindebtedness and the reckless behaviour of some lenders in extending loans to consumers who cannot afford them.”

In the unsecured-lending market, “some lenders tend to lend at the maximum rates”, said Selibi, citing the regulator’s internal research.

This was also evident from complaints it received.

According to the MFSA’s Ferreira, however, it varied a great deal. Something in the region of 18% of short-term and unsecured credit would be affected by the lowering of rates, he told City Press.

This effect will probably be small when it comes to mortgages. Banks generally do not charge the maximum permitted rates on home loans. With short-term and unsecured loans, the situation is different. Retailers also tend to charge precisely the maximum on their store cards.

Rob Jeffreys, MD of consultancy Econometrix, said that government had in effect introduced price control on credit. He had done commissioned work for the MFSA, which made the case for “substantial” increases in the maximum rates and fees.

The fee increases being proposed were “completely incongruous”, he told City Press. Inflation alone meant they should rise at least 70%, not 5%, he said. “The maximum interest rate should go up, not down.”

How the repo rate is affected

Monetary policy at a glance

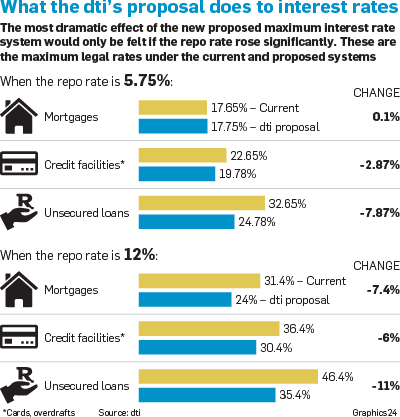

New interest rate proposals by the department of trade and industry (the dti) will fundamentally change the way in which the SA Reserve Bank indirectly sets maximum interest rates in the entire consumer credit market, including home loans, with its all-important repurchase (repo) rate.

This is happening just as South Africa enters an upward cycle in interest rates after the repo rate reached a low point of 5.5%. The dti is in effect planning to make the looming repo rate increases less powerful as a determinant of interest rates faced by consumers.

It currently works as follows: The maximum legal interest rates in South Africa are set according to a formula based on the repo rate. Every 1 percentage point hike in the repo rate makes all the legal maximum interest rates in the country rise by 2.2 percentage points.

The dti’s proposal is that a 1-point hike in the repo rate makes the legal limits go up by only 1.7 points.

For the largest debt market, mortgages, the proposal is more extreme: every 1 point of repo rate increase will translate into only 1 point in the maximum rate.

This will in effect reduce credit providers’ ability to pass on the soon-to-rise cost of capital to consumers paying the highest rates.

The effect of this on banks and other credit providers can become spectacular if the repo rate goes back up to anything like the 12% it reached in 2008.

According to the National Credit Regulator’s Lebogang Selibi, the proposals “are meant to support monetary policy” and the lowering of the effect of the repo rate on maximum rates has been proposed before to make monetary policy less pro-cyclical.