Publications

Publications

Partners

Partners

Some might find the timing of this article ironic considering developments around the #FeesMustFall movement. But whether tertiary education fees will fall or not, and in the absence of a crystal ball to predict the future, the best we can do is plan and be prepared.

Tertiary education might be free in future, but of what quality will it be? Will its qualifications be recognised overseas? Or you might consider sending your child to an overseas institution – inevitably this will be expensive.

South Africans are very bad at saving for retirement, but it doesn’t end there: we are bad at saving, period. This includes a lack of saving for our children’s future education needs. According to figures from the 2015 Old Mutual Savings and Investment Monitor, 60% of those surveyed said they don’t save for their children’s education, and 54% of parents said they are not aware of the future costs of education.

This in itself represents a problem, because while the long-term average inflation rate hovers at around 6% a year, the education inflation rate is closer to 9%. Education inflation constantly outstrips general inflation, and if you understand the power of compounding, you will realise that it’s a significant difference.

According to an article on businesstech.co.za, it costs between R29 000 to R62 500 per year for a BCom degree and R30 600 to R64 500 for a BSc degree, depending on the university.

Of course, living expenses also have to be taken into account. A Google search for living costs for a student at the University of Cape Town (UCT) reveals that you can add approximately R130 000 a year for rent, food, transport, books, etc.

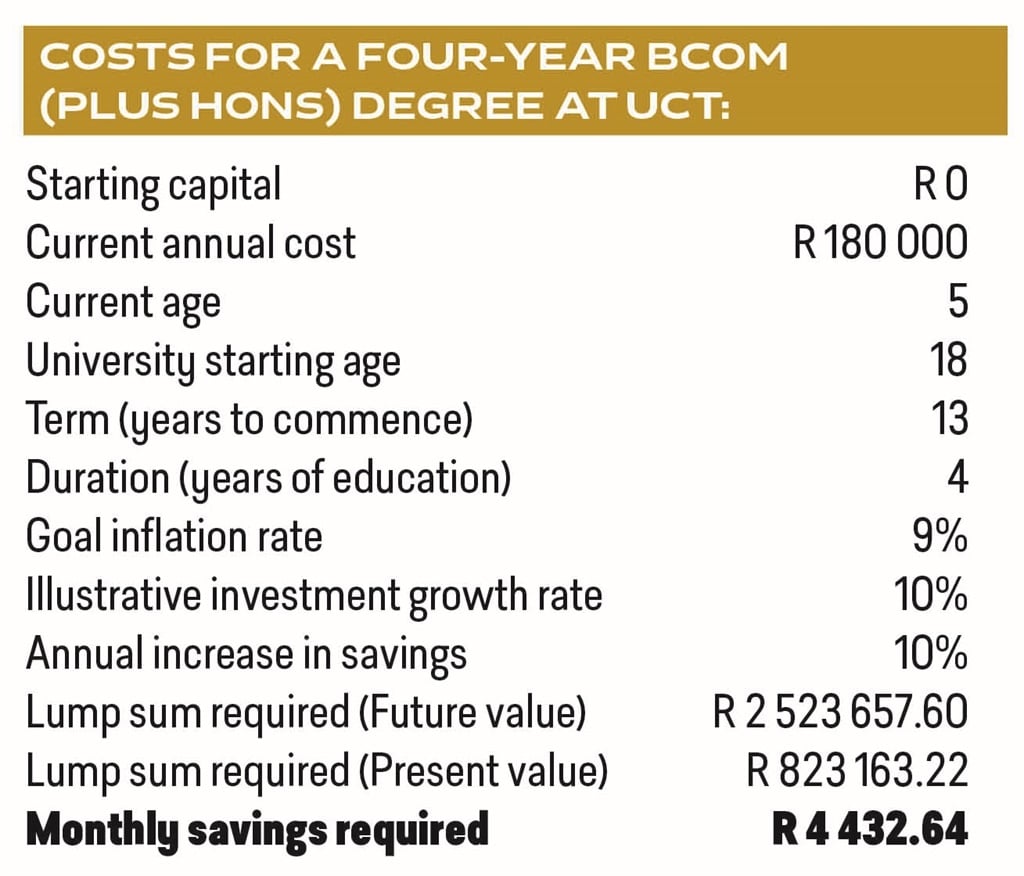

You will therefore need between R180 000 to R200 000 a year in today’s money if your child also needs accommodation in order to study a BCom Honours degree at UCT.

So, if your child is now five years old and you haven’t started saving yet, you will have to start by putting away approximately R4 400 a month (increasing at 10% a year) from now until the child is 18 to reach the goal of R180 000 a year for four years of study. This equates to a lump sum of ?R2.5m in 13 years’ time to cover all expenses (see below).

The costs highlighted here illustrate why it is so important to start saving for education as early as possible, but also to save correctly. As mentioned, education inflation averages 9% a year, so simply putting money away into a savings account won’t be sufficient. Education savings, just like retirement savings, need exposure to higher growth asset classes like equities and listed property over the long term in order to meet its objective.

It is also important to remember that the time horizon for education savings is much shorter than saving for retirement, so you will need to start saving as early as possible. Exposure to the more risky asset classes like equity and listed property will also have to be gradually reduced the closer you get to the time that your child is going to university in order to avoid possible capital losses without sufficient time for recovery.

At this point you might be wondering what the best savings vehicle is to use in order to save for your child’s tertiary education. With the launch of tax-free savings accounts last year, you can save up to R30 000 a year, and R500 000 over a lifetime, and all growth on the investment is tax free. This means there is no capital gains tax, and also no tax on dividends and interest, adding substantially to the overall investment returns.

A tax-free savings account giving you exposure to collective investment schemes with access to equities and listed property, in your child’s name, is a great way of starting to save for your children’s tertiary education needs. Just be aware of the R500 000 lifetime contribution limit. When it’s been reached, your children will not be able to contribute in their own name in future.

And if after reading this you feel that you can’t afford your child’s future tertiary education, just remember that with proper financial planning it is possible – even if fees don’t fall.

Rupert Giessing is a director at Vista Wealth Management, a representative under supervision of Accredinet Financial Solutions.

This article originally appeared in the 17 November edition of finweek. Buy and download the magazine here.